Global Broker Regulation Inquiry App

WikiFX

English

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

Opportunities in Oil as Gold Pulls Back - Week 45| Technical Analysis by Jasper Lawler

Abstract:Week Ahead10–16 November 2025Global markets entered mid-November on shaky ground after a tech-led pullback knocked the SP 500 off record highs and mixed US data clouded growth amid the government shut

Week Ahead

10–16 November 2025

Global markets entered mid-November on shaky ground after a tech-led pullback knocked the S&P 500 off record highs and mixed US data clouded growth amid the government shutdown. Focus shifts to key UK and China data, a busy UK earnings slate, and Fed rate-cut odds near 65% for December.

Week in Review

Central banks:

The BoE held rates in a close split, showing a live debate on cuts. The RBA also paused with a cautious tone. Fed Chair Powell, after October‘s 25bp cut and QT wind-down hint, warned a December move isn’t assured.

US data gap:

With official data halted, private indicators filled the void: ADP showed +42k jobs, Challenger layoffs hit 153k, and the Chicago Fed saw unemployment at a four-year high.

Earnings:

Despite equity jitters, Q3 results stayed solid—82.5% of 446 S&P 500 firms beat estimates, the best since mid-2021.

Price Action

Equities:

S&P 500 slipped ~2.4% from its Oct 28 peak, led by a 6% tech drop. The FTSE 100 held firmer on a weaker pound.

Commodities:

Oil eased on inventory builds and OPEC+ talk; gold steadied after a 10% slide as yields cooled.

FX:

GBPUSD fell toward 1.30, yen gained on risk aversion, and NZD weakened on soft local data.

Themes:

AI-driven stocks corrected, gold‘s pullback trimmed hedge demand, and sterling’s weakness supported FTSE exporters. Crypto stayed subdued, capped by key resistance after Octobers shakeout.

Week AheadEarnings Calendar

Vodafone (H1 FY26) – Monday, 11 Nov:

Modest recovery from multi-decade lows. Watch German turnaround, synergy delivery from the Three merger, and confirmation of FY26 guidance (underlying cash profits €11–€11.3bn; FCF €2.6–€2.8bn). €500m buyback in focus.

Cisco (Q1 FY26) – Wednesday, 12 Nov:

Cisco reports amid volatility in tech. Last quarter revenue fell 3% to $13.5bn, with software and security offsetting weaker hardware demand. Focus on AI-driven data-centre orders and signs of a second-half rebound.

Rolls-Royce (Q3 FY25) – Thursday, 13 Nov:

Shares near record highs ~1,200p. H1 underlying op profit +50% to £1.7bn; FCF £1.6bn; guidance raised. Civil aero margin ~25% the engine. SMR funding plans remain a watchpoint; IPO talk denied.

Burberry (H1 FY26) – Thursday, 13 Nov:

Turnaround under “Burberry Forward” targeting £80m savings. Q1 revenue -6% to £433m; Asia soft, US +4%. Evidence of margin traction and brand momentum in focus.

Disney (Q4 FY25) – Thursday, 13 Nov:

Parks and cruises strong; content softer. Q3 EPS $1.61; Disney+ +1.8m subs. Watch cost discipline and franchise slate guidance.

Economic Calendar

UK Wages/Unemployment (Sep) – Tuesday, 11 Nov:

Jobless rate has risen from 4.0% to 4.7% y/y; wage growth holding ~4.7% with public-sector strength. Sticky pay keeps BOE constrained ahead of the Budget and amid IMF warnings on UK living standards.

UK GDP (Q3) – Thursday, 13 Nov:

Monthly GDP +0.1% in August after a -0.1% July revision; services flat. Manufacturing/industrial gains may support Q3, but momentum remains fragile.

China CPI (Oct) – Sunday, 10 Nov:

Seen slipping back into deflation around -0.1% y/y, raising stimulus hopes.

China Retail Sales (Oct) – Friday, 14 Nov:

Seen easing to ~2.2% y/y from 3.0%, implying softer consumption.

Australia Unemployment (Oct) – Thursday, 13 Nov:

Tight but cooling labour market as RBA stays cautious.

EU GDP (Q3, 2nd) – Friday, 14 Nov:

Confirms modest growth amid weak manufacturing.

US data note:

CPI, PPI and Retail Sales are likely to be delayed by the shutdown.

Technical Analysis

We look at hundreds of charts each week and present you with three of our favourite setups and signals.

USD/CADSetup

Bullish breakout

Completed an inverse H&S bottom

Broken above 1.40 but not cleared 1.41

Daily moving averages in bullish alignment

Commentary

Despite the highest weekly close in months, there was hesitation at 1.41 - offering the chance for a pullback trade.

Strategy

Buy pullback near 1.40

A close below 1.39 would indicate a deeper correction

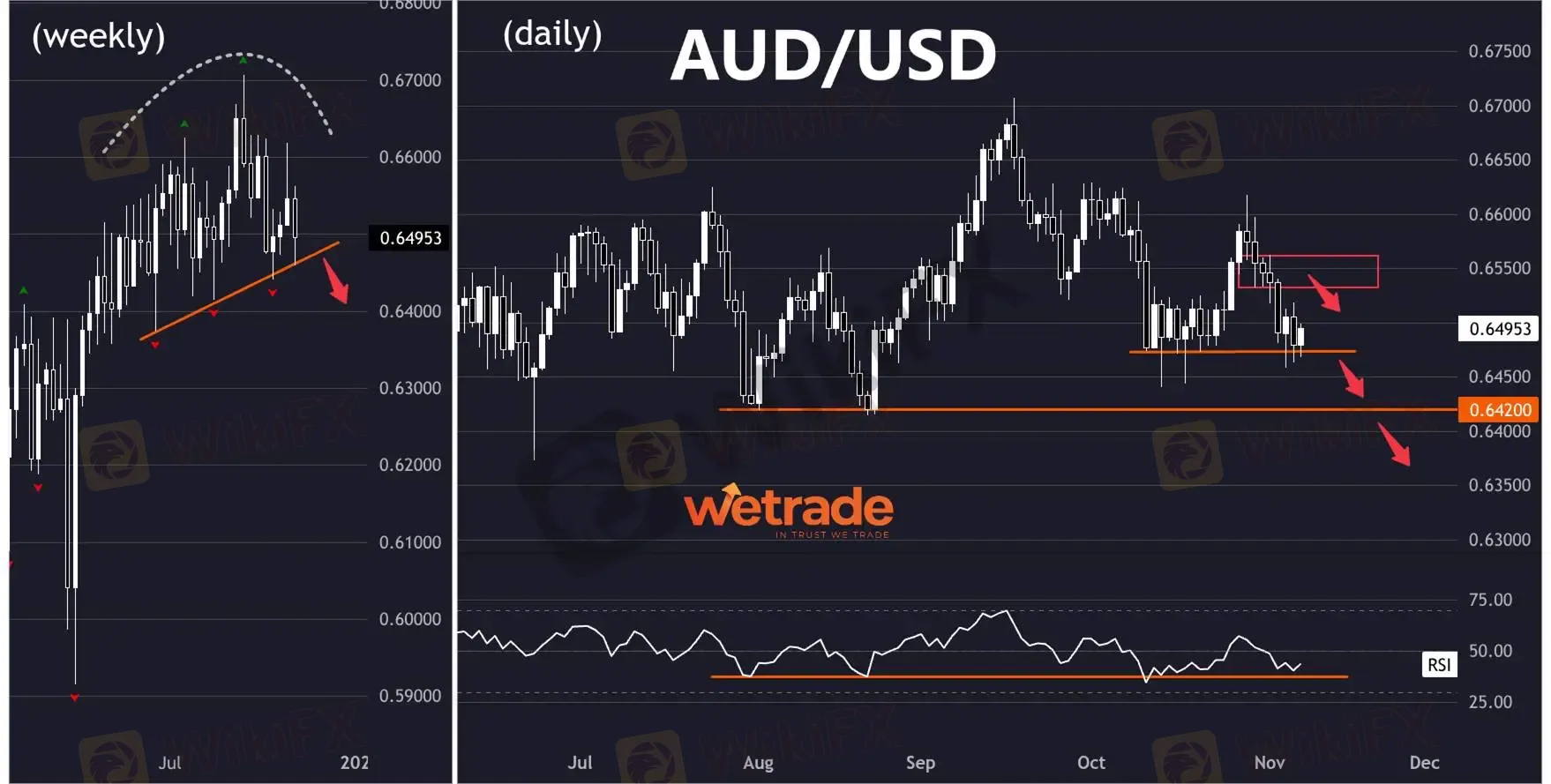

AUD/USDSetup

Need a break of the weekly uptrend line to turn bearish

Solid support from 0.64-0.65

Commentary

Strategy

Look for bearish setups after a close below 0.65

Buy if there is a strong move off support at 64

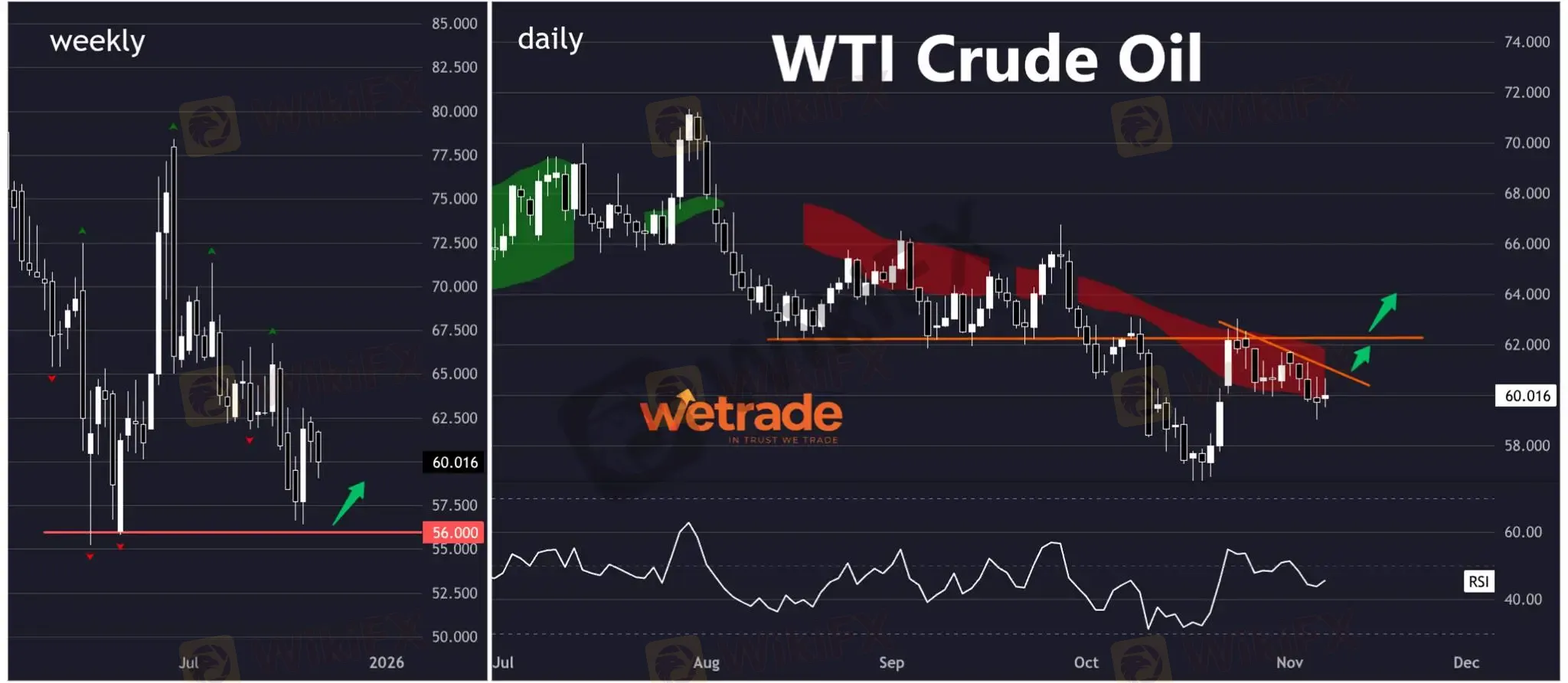

WTI Crude OilSetup

Bullish engulfing weekly candle off 56.0 support

Daily trend is still down - looking for bullish break

Commentary

Strategy

Aggressive: Buy bull flag breakout

Conservative: Wait for bullish setups after break over 62

Range market - possible bearish reversal

The weekly price action looks more like a top than a continuation. Our bias is towards a bearish break, but we will be cautious about any bearish trades before support breaks.

NOTE: Look out for bullish reversal from 0.64 (bottom of the range)

Bullish reversal off long-term support

Looking to trade in line with signs of new bullish momentum. A close above 62 (support-turned resistance) would confirm a new bullish bias.

But - as always - thats just how the team and I are seeing things, what do you think?

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

Forex Expert Recruitment Event – Sharing Insights, Building Rewards

WikiFX

WikiFXAdmirals Cancels UAE License as Part of Global Restructuring

WikiFXMoomoo Singapore Opens Investor Boutiques to Strengthen Community

WikiFXOmegaPro Review: Traders Flood Comment Sections with Withdrawal Denials & Scam Complaints

WikiFXAn Unbiased Review of INZO Broker for Indian Traders: What You Must Know

WikiFXIs Fyntura a Regulated Broker? A Complete 2025 Broker Review

WikiFXPINAKINE Broker India Review 2025: A Complete Guide to Safety and Services

WikiFXIs Inzo Broker Safe or a Scam? An Evidence-Based Analysis for Traders

WikiFXIs Uniglobe Markets Legit? A 2025 Simple Guide to Its Safety, Services, and User Warnings

WikiFXIs Forex Zone Trading Regulated and Licensed?

WikiFXCurrency Calculator

USD

CNY

Current Rate: 0

Amount

USD

Available

CNY

Calculate